2018 was the biggest year for my finances and probably for my life so far. In 2018 I became debt free and I was also made redundant. I’m very proud of what I managed to achieve in only 12 months though. Have a read to find out everything that went on in 2018…

If you’d like to skip to a particular category of this report click the links below:

Debt Payoff | Savings | Spending | Earnings | Superannuation| Credit Score| Shares

Debt Payoff

I started 2018 with a debt of $6,331 (AUD). This was for my personal loan which was initially a car loan that I’d consolidated into my personal loan. I had transferred it to a Citibank 0% interest credit card in November 2017. I found it much easier to pay off without having interest payments adding to it. Consolidation is not always a great idea so definitely speak to a financial expert before doing anything.

I continued to save as much as I could from working 2 jobs, 6-7 days a week and also by cutting down on my expenses. You can read more in each of my monthly reports on what I was spending and what percentage I was putting towards debt. I was aiming for about 30% of my income to go towards debt/savings. If this isn’t possible for you just try and put aside as much as you can. You can read more about how I paid my debt in my “I’m debt free” post.

By 15th June I made my final payment and become debt free. I was incredibly proud. It was the first time in my adult life I had ever been debt free.

I had paid off $11,489 in 12 months.

Savings

After paying off my debt my next task was to begin saving. I wanted to save up a 3-month Emergency fund (EF) as well as just grow my savings in general. Before I was made redundant I had $4,720 saved which I’d saved between June and August. In October I received the payment and I completed my 3-month EF ($12,000). I put the rest into savings and my balance became $28,877. I had to live on my savings for 1 month before I was able to get a new job. By the end of 2018, my savings balance was down to around $21,900.

I had spent several thousand in the last few months of 2018 getting my wisdom teeth removed, moving house (paying for a new bond etc) as well as getting a new tattoo. I also purchased a new TV, a coffee table and let myself spend some money as I hadn’t done too much spending in months! In hindsight I could have spent less but I feel ok about it. (you do you)

In total for the year I saved $33,941 which was 38% of my income.

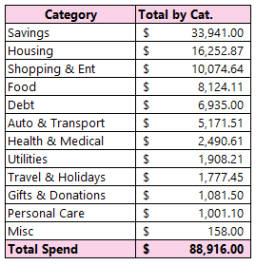

Spending

Below is my 2018 spending by category. Now I wouldn’t class savings as ‘spending’ really but I wanted to have accurate percentages of where my money went overall. If you minus the spending and debt categories from the total then my spend becomes around $48,000. I’m happy that 38% of my pay went to savings and 8% went to debt. Keep in mind the debt was only for 6 months of 2018.

Below is a breakdown of my spend by month. October ($5,286) was my biggest spending month which was no surprise to me as it’s when I received my payout and went a little bit overboard on spending. My lowest spend month was February ($2,977).

Each month I tried to cut back on certain expenses as that’s a great way to ‘find’ extra money to put towards debt. I could have done better and this year I’m trying to spend less on food and shopping. Keeping track of your spending can really help you see where your money is going and where you can cut back. I now try and write down my spending every day so that I know exactly where it’s going.

Earnings

The sweet stuff! It seems everyone wants to know what other people earn. Now I’m not going to tell you every little dollar of what I earned (I’ve got to have some secrets right?) However, I am happy to tell you the different ways I earnt money. The key to paying back debt and creating savings is to cut back on expenses but also to increase your income. Having multiple avenues of income is the key to creating wealth. I want to be able to increase my income streams in the future. If you’ve got any tips on how I can create more income let me know.

My Income Streams

(in no particular order)

- Main income from my full-time job

- Pure Profile (survey site)

- Google Rewards (survey app)

- Valued Opinions (survey site)

- Field Agent (app)

- Purkle (survey site)

- Container refund scheme

- Casual retail job (I don’t work there anymore though)

- Selling items on Facebook Marketplace

- Interest from savings account (I use ING and get 2.8%)

- Redundancy payout

- Gift card promotions (e.g Finder, ING gift card)

- Shopback rewards

- Free money promotions such as with Spaceship

- Tax Return

My side hustles accounted for 10% of my total income. If you exclude my payout they accounted for about 16% of my income.

Below you’ll find a breakdown of my total income per month. October was very high because that’s when I received that payout. Other than that it’s pretty consistent across the year.

Superannuation

Superannuation wasn’t a major focus of mine for 2018. Paying off debt and saving money came first. In 2019 I do want to start to put money into it though. I may only be 28 but I want to be able to have a great retirement.

In 2017 I changed my super over to Hostplus as it has lower fees and a good return. Do your own research before making any changes though (I’m not qualified to give financial advice). I read “The Barefoot Investor” which recommends Hostplus and I was happy to change based on my research. You can read more about my experiences with the book here.

During the year I changed my investment options accidentally and it caused a drop in my balance. I think the share market also had something to do with it as we all know it wasn’t doing too well at the end of last year.

Below is a visual of my super balance from June-December.

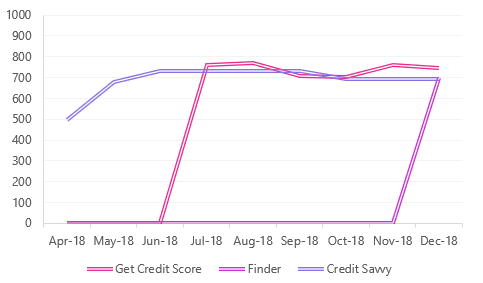

Credit Score

During the year I started to check my credit score. I began by using the Credit Savvy website and then in July I also started comparing it to the Get Credit Score website. In December I also used the Finder website.

You’ll find that all of the sites give you different scores so it can be helpful to get an average from across them. Below is my score for each website across the whole year. Two of them are very close. Ignore the 0 values as I didn’t start using some of them until later.

Do you know what your score is? If you don’t feel free to check yours with Finder via this link for free and you’ll also get a $5 woolworths gift card just for checking your score. Just so you know, I’ll also get a $5 gift card too!

Shares

Having shares was always a financial goal of mine and in November 2018 I finally purchased my first lot of shares.

The market wasn’t great at the end of last year and my balance did initially drop but it’s now back over what I paid for them. I do want to learn more about shares before I purchase my next lot. I’m in it for the long haul though and I want to grow my investments for the future.

In terms of micro-investing, I also have a Spaceship account. I took advantage of an opening bonus offer that they had where if you put in $10 you received $20. I haven’t taken the money out of the account and it’s slowly growing.

2018 Monthly Reports

Just in case you’re interested below are my monthly reports for 2018. There was no report for April as I was touring North QLD for Tour De Cure and didn’t really have the time to get a report out.

January | February | March | May | June |

July | August | September | October | November | December

I hope you liked this overview of 2018. Let me know how 2018 was for you in the comments below. I’d love to know how much debt you paid or savings you accomplished in 2018.

I am in the United States of America. I don’t know how to interpret your income. Can you give us a frame of reference? Tell us how much things cost in where you live, such as groceries, houses, and cars. Perhaps, tell us how much certain jobs pay, such as minimum wage, grocery store clerk, etc.

LikeLike

Hi there,

My blog is mainly for Australian readers. It may help to change it to US$ with google.

In terms of frame of reference all those vary so much by state. Minimum wage is around $700/week I believe and you’d be able to get at least $25/hr as a grocery worker. We definitely have better pay then the US. Our cost of living is higher though with an average house in places like Sydney costing over $1million. You could get a decent home in my area for about $500,000 I think. Cars I’m not sure about as it varies but I purchased mine second hand for $13,500. In terms of groceries we don’t coupons like you do so things cost more. Milk approx $1/litre, bread $1/loaf, eggs $4/12 pack, chicken $9/kilo.

Does that help?

LikeLike

Thank you! When I first found your blog, I thought, “Wow, with income like that, of course she is debt free!” You expressed rather high income/expenses for your age. Later, I realized that you were not in the US.

In the US, minimum wage is $7.25. I assume young grocery workers earn about that much. Home prices vary widely based on location. A 3-bedroom house in a suburban/rural location on reasonably small piece of land might be in the $150,000-$300,000 range. New cars are $25,000-$45,000. Three year old used cars are $10,000-$15,000.

Good for you for being frugal. Keep up the good work! Thank you for sharing your story.

LikeLike